Estimated Income Tax Payments

IRS, State

Estimate Payments

Key points on this page:

- The simple rule of thumb is that if you expect to owe at least $1,000 in taxes when you file, you should make estimated tax payments to lower this figure or at least bring it below $1,000.

- If you have income without taxes withheld, you likely owe estimated taxes and should make them quarterly.

- Pay the IRS and/states online rather than mailing in payments.

- How to report IRS tax estimate payments on your eFile.com tax return

Important: Send your estimated tax payments to the IRS online so you do not have to mail Form 1040-ES. On the IRS payment page, select Estimated Tax and the platform will select 1040-ES so you can submit the 1040-ES tax payment online without having to mail a check or fill in any forms.

Pay estimated IRS taxes online:

Pay IRS Taxes

Estimated income tax payments are made to pay taxes on income generated in a given tax year that is not subject to periodic tax withholding payments, such as wages are via the W-4 form. Generally, if you are an employee whose only income is from a W-2 with taxes withheld, you will not have to worry about making estimated income tax payments as this is done through your employer. Independent contractors or self-employed individuals must make IRS and state tax estimate payments. The taxpayer makes Quarterly estimated tax payments so they are not in significant debt to the IRS. If a taxpayer did not make sufficient tax estimate payments for a given tax year, the IRS might add tax penalties based on the submitted tax return. Generally, the IRS may assess penalties if you owe more than $1,000 on your tax return.

As of January, taxpayers start planning and making estimated tax payments for the current tax year. This prepares them for their returns in the following year.

Read this IRS Publication on Tax Withholding and Estimated Tax Payments for detailed information and estimate your taxes with the free tax return estimator.

Who Should Make Estimated Tax Payments

The most common taxpayers who are subject to making estimated tax payments are the self-employed, who may receive income on a 1099 form, such as a 1099-NEC. If you receive taxable income with no tax withheld, you are responsible for making these income tax payments independently, as you do not have an employer to do this for you. Employees who receive a W-2 have their taxes withheld based on the W-4 withholding form they submit. 1099 employees do not have this and should make estimated payments so they do not owe tax penalties at the end of the year.

If a taxpayer generates the following types of income throughout a given tax year, it may be subject to estimated income tax payments via periodic payments:

See a general list of taxable income types.

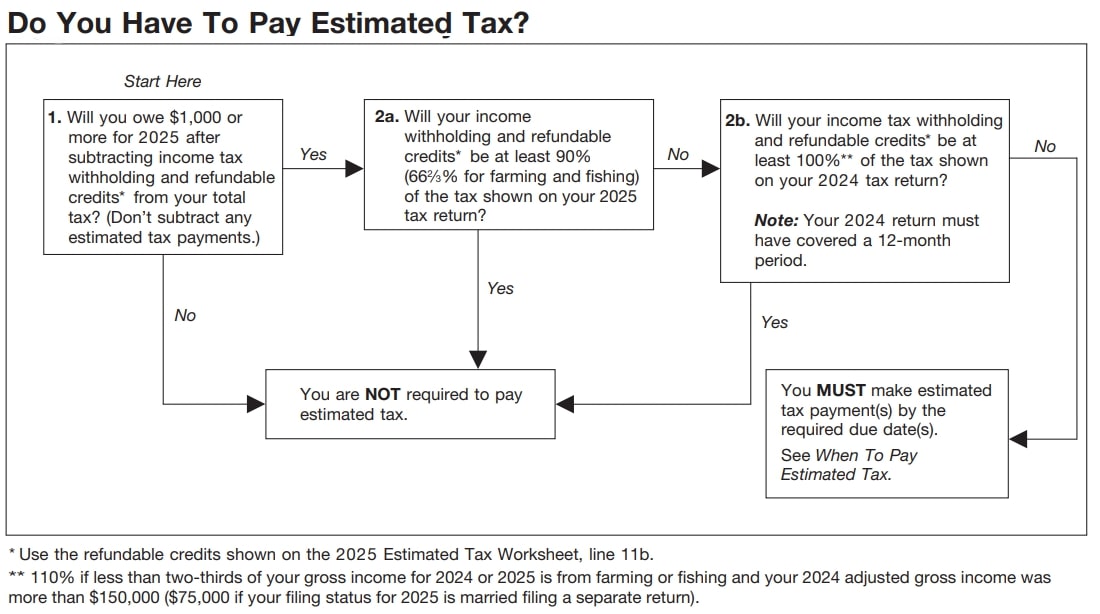

Click on the image above for a high-level overview of tax estimate payments to determine if you need to pay estimated taxes. Here are the general guidelines on who should make estimated income tax payments:

- The expected income tax amount for the given tax year is at least $1,000 after deducting withholding and tax credits. This is when you expect to owe at least $1,000 when you file.

- Tax withholding and tax credits are less than the smaller of:

- 90% of the expected taxes on your current Tax Return, or

- 100% of the taxes shown on your previous Tax Return.

- In other words, you can use your exact figure from your previous year's return or estimate within 10% of your anticipated tax balance.

- Use the free Tax Return Estimator to estimate your income taxes.

Pay Estimated Taxes Online: IRS or Federal | State(s)

Of course, these are just estimated. If you underestimate by a small enough amount, you should not owe penalties and will simply owe the difference in tax when you prepare and file your Tax Return. If you overestimate, you will be owed a tax refund, similar to when an employer withholds too much tax during the year. When you prepare your return on eFile.com, you can input the estimated tax payments you have made. The eFile Tax App will put them on your return and help you determine if you owe additional tax or if you are owed a tax refund.

Payments can be made close to these dates, but taxpayers may find it easiest to make payments around the due date. That way, they can keep a consistent schedule. If you are unsure how much in estimated tax payments you should make, use the free tax return estimator. Once you get your answer, divide the total taxes due by four, and these are your four tax payments.

Taxpayers whose income is subject to estimated withholding should make their estimated payments by these dates:

- April 15 for income earned January 1 - March 31

- June 15 for income earned April 1 - May 31

- September 15 for income earned June 1 - August 31

- January 15 of the following year year for income earned September 1 - December 31.

The due dates for each year are always April 15, June 15, September 15, and January 15 unless the IRS extends the deadline, perhaps due to disaster situations.

Estimated Tax Payment Guidelines

Like most taxing guidelines, there are exceptions to making estimated tax payments. The points below will help determine if you should make estimated tax payments for any year.

- A: Will you owe $1,000 or more for the tax year after subtracting income tax withholding and tax credits from your total tax? Do not subtract estimated tax payments! If yes, read B. If no, then estimated payments are not required, but making these throughout the year may be a good idea so you do not pay it all at tax time.

- B: Will your income tax withholding and tax credits be at least 90% of the tax shown on your next tax return (66.33% for farmers and fishermen)? If yes, no estimated tax payments are required. If no, read C.

- C: Will your income tax withholding and tax credits be at least 100% of the tax shown on your last tax return? In other words, will your current withholding and credits cover your tax liability? Find out using this free tax calculator; if not, you must make estimated tax payments.

Additionally, the key points below apply to specific situations:

- You were a U.S. Citizen or resident alien during the year and had no tax liability for the entire 12-month tax year. No tax liability for the year means your tax was zero, or you are not required to file an income tax return. Thus no estimated payments are needed.

- There are special rules for farmers, fishermen, certain high-income individuals, and certain household employees.

- If a majority of income is from farming or fishing, the 90% guideline above is lower at around 66%.

- Household employees will want to work with their employer to see how their taxes will be handled (if they have tax withheld from other income, if they would be required to make estimated payments, if household employment taxes were excluded, etc.). Generally, if you pay a household employee cash wages of $2,600 or more in 2023 (up from $2,400 in 2022), you, as the payer, must withhold tax withholding. See the IRS Household Employer's Tax Guide.

- If your Adjusted Gross Income (AGI) was greater than $150,000 $75,000 for married filing separately, you should make payments if your estimated withholding and credits are less than 110% of your taxes (instead of 100%).

- For more details, see instructions on Form 1040-ES and IRS Publication 505, Tax Withholding and Estimated Taxes.

- We recommend making estimated IRS tax payments via the Pay Estimated Taxes links above.

When you owe taxes through quarterly payments, make these online so you do not have to mail Form 1040-ES with payment. The payment goes through within the same day, and you do not have to worry about sending a check through the mail. Pay IRS taxes online for convenience and security.

Where to Mail Estimated Tax Payments or 1040-ES

It is much safer and easier to pay your estimated taxes online, but the addresses below are where you should mail your Form 1040-ES with payment based on your resident state.

Arkansas, Connecticut, Delaware, District of Columbia, Illinois, Indiana, Iowa, Kentucky, Maryland, Maine, Massachusetts, Minnesota, Missouri, New Hampshire, New Jersey, New York, Oklahoma, Rhode Island, Virginia, West Virginia, Vermont, Wisconsin

Internal Revenue Service

P.O. Box 931100

Louisville, KY 40293-1100

Alabama, Arizona, Florida, Georgia, Louisiana, Mississippi, New Mexico, North Carolina, South Carolina, Tennessee, Texas

Internal Revenue Service

P.O. Box 1300

Charlotte, NC 28201-1300

Alaska, California, Colorado, Hawaii, Idaho, Kansas, Michigan, Montana, Nebraska, Nevada, North Dakota, Ohio, Oregon, Pennsylvania, South Dakota, Utah, Washington, Wyoming

Internal Revenue Service

P.O. Box 802502

Cincinnati, OH 45280-2502

A foreign country, U.S. territory, use an APO/FPO address, file Form 2555, or if you are a dual-status alien.

Internal Revenue Service

P.O. Box 1303

Charlotte, NC 28201-1303

USA

How to Estimate Your Taxes Owed

The simplest way to determine how much you should pay in estimated taxes is to use the free tax calculator to estimate your next return. Then, take your total taxes due for the year and divide them by four: these are your four quarterly payments. Follow these tips below:

Start with the free eFile.com Tax Calculator and estimate your income and taxes for the year:

Tax Year Calculator

- If your income situation is similar to the prior year, make estimated payments based on this. For example, if you owed taxes last year and your income is around the same this year, consider making slightly larger estimated tax payments so you do not owe when you file.

- If you also receive W-2 income in addition to the income types listed above, you can increase your federal tax withholding via Form W-4 to offset your income that does not have taxes withheld. The W-4 form has a line that allows you to withhold an additional income tax amount. Use the eFile.com W-4 TAXometer to calculate the calendar year tax return's withholding.

- If your income changes throughout the year, you should make estimates based on the annualized income installment method. See instructions on Form 1040-ES or IRS Publication 505 on Tax Estimates, Chapter 2.

- The IRS may apply a penalty if you didn’t pay enough estimated taxes for the year, didn’t pay the required estimated amount, or didn't pay on time.

IRS and State Estimated Tax Payment Methods

TurboTax® is a registered trademark of Intuit, Inc.

H&R Block® is a registered trademark of HRB Innovations, Inc.